Protect

Plan

Grow

The Essential Importance of Trust

Are you ready to secure your family's financial future and protect your assets?

The essential importance of trust cannot be overstated. Setting up a trust helps you achieve the following crucial benefits:

Avoid the lengthy and costly probation process

Protect your assets from creditors

Qualify for certain government benefits

Maintain privacy regarding your assets

Minimize your gift and estate taxes

Shift income and minimize your income tax

Set specific parameters for the use of your assets

What is a Trust, and How Does it Work?

A trust is a legal arrangement in which one party, known as the grantor or settlor, transfers assets to another party, known as the trustee, to hold and manage for the benefit of one or more beneficiaries. There are many types of trust, but there are only two broad categories of trusts:

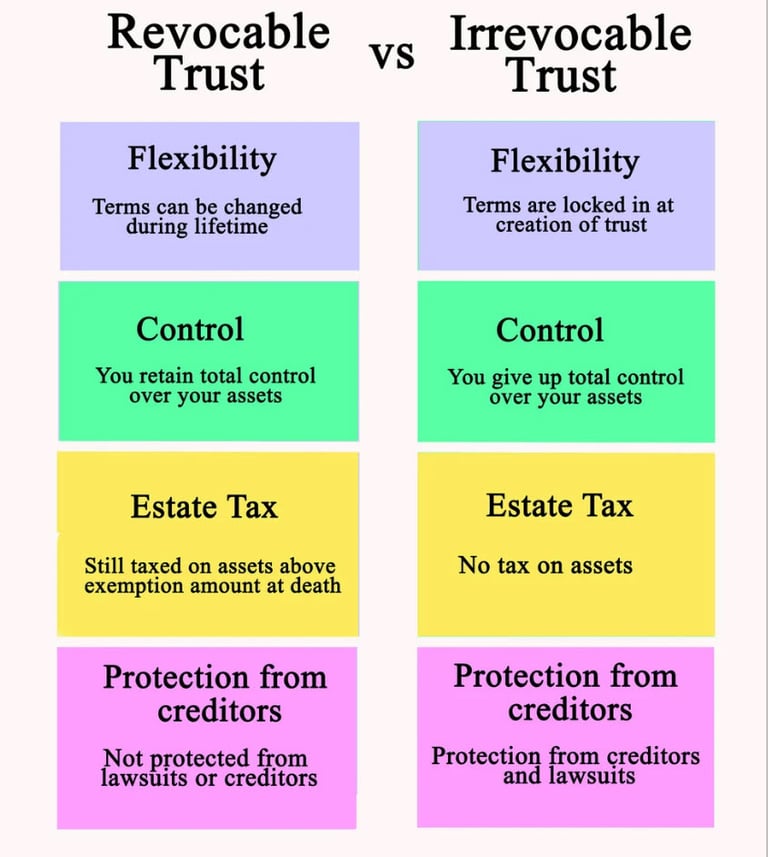

A revocable trust, which can be dissolved or changed by the grantor at any time. A revocable trust can accomplish many of the same things as a will. However, there’s one key difference. “ In California, a trust avoids probate, while a will does not. Further, the net income of trust is taxed to the grantor, and the trust assets are not protected from creditors and includible in the gross estate of the grantor

An irrevocable trust, which cannot be changed once it has been created. The trust assets are non-includible in the gross estate of the grantor and are generally protected from creditors. However, the tax treatment of income generated from assets transferred into the trust depends on the trust's specific terms and whether it is classified as a grantor or non-grantor trust for tax purposes.

Will vs. Trust: What are the Key Differences?

Wills and trusts are legal documents that direct the distribution of your assets after your death to your designated heirs and beneficiaries. However, trusts provided the following additional benefits:

Avoid the lengthy and costly probation process: In California, a “Last Will & Testament” does NOT prevent you from having to go through probate, while a “trust” avoids probate. The probate process can be time-consuming and expensive, so many people try to avoid it by setting up a trust. Probate fees in California are calculated based on the estate’s gross value. In 2023, the rates were 4% for the first $100,000, 3% for the next $100,000, 2% for the following $800,000, 1% for the next $9 million, and 0.5% for the next $15 million. Further, in California, typically the probate process takes 12 to 18 months, though larger or more complex estates can take even longer.

Protect your assets from creditors: An irrevocable trust can protect your assets from creditors because when you transfer the properties into the trust, you no longer legally own those properties. The irrevocable trust is a separate legal entity that holds the transferred assets, which are managed by a trustee.

Qualify for certain government benefits: A Medicaid asset protection trust (MAPT) can be useful for estate planning if you believe you or your spouse will need long-term care at some point. Transferring assets to this type of trust can allow you to qualify for Medicaid to pay for long-term care while preserving your savings. If you don’t have a long-term care insurance policy in place, you may consider adding a Medicaid trust to your estate plan.

Maintain privacy regarding your assets- With a will, the distribution of your assets is a matter of public record. However, with a trust, the distribution of your assets can be kept private. This makes it possible for an assigned individual to take over for you if you should become incapacitated.

Minimize your gift and estate taxes - An irrevocable trust, however, is one that you cannot usually change after the agreement is signed. Because you’ve transferred assets out of your estate, there may be transfer tax benefits with an irrevocable trust. Contributions to the trust are generally subject to gift tax requirements during your lifetime. However, if certain conditions are met, assets placed in this type of trust (and appreciation on those assets over time) will be sheltered from estate tax after your death. In addition to initial funding, you can make an annual exclusion gift to an irrevocable trust each year without having to pay additional gift tax on that contribution. The 2024 gift tax exemption rate is $18,000 for individuals or $36,000 for married couples filing a joint return.

Shift income and minimize your income tax - For example, certain types of trusts can be used to shift income to beneficiaries in lower tax brackets, thereby reducing the overall tax liability.

Set specific parameters for the use of your assets- trusts give you the ability to truly customize your estate plan. You can include conditions such as age attainment provisions or parameters on how the assets will be used. For example, you can state that you’d like the money in a trust to be given to your grandchildren only once they turn 18 and only to be used for college tuition.